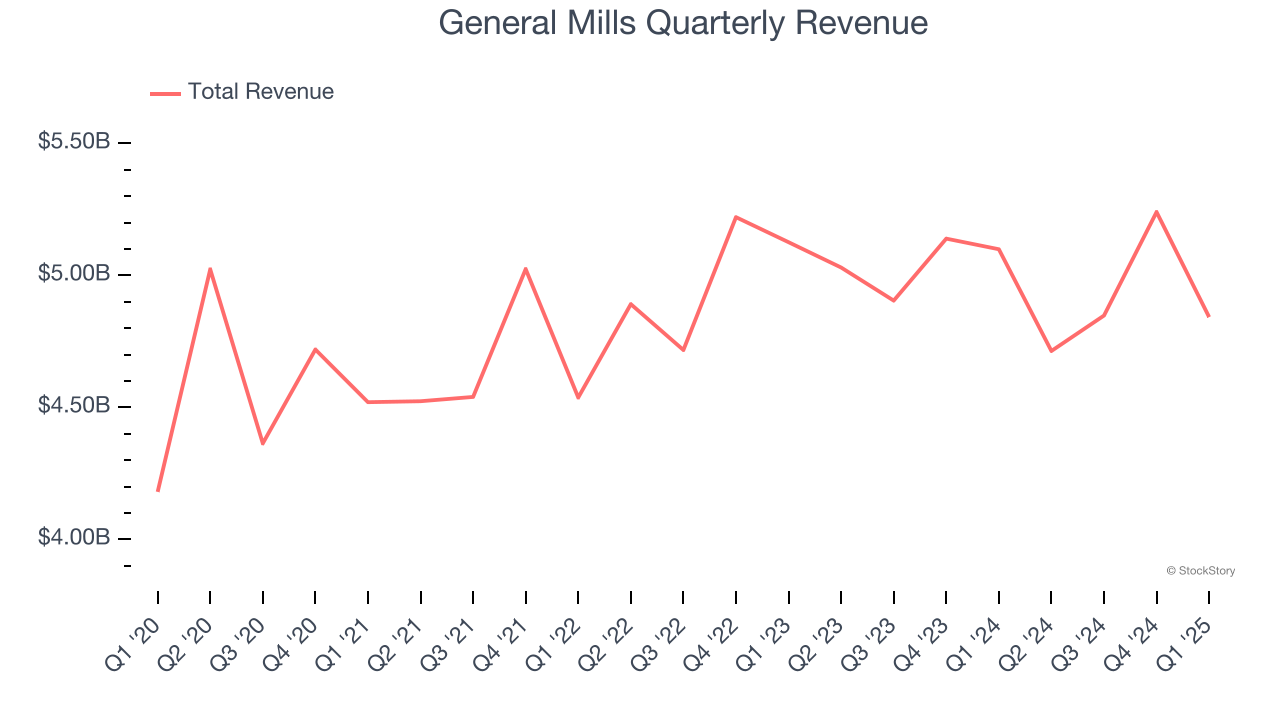

Packaged foods company General Mills (NYSE:GIS) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 5% year on year to $4.84 billion. Its non-GAAP profit of $1 per share was 4.1% above analysts’ consensus estimates.

Is now the time to buy General Mills? Find out by accessing our full research report, it’s free.

General Mills (GIS) Q1 CY2025 Highlights:

- Revenue: $4.84 billion vs analyst estimates of $4.96 billion (5% year-on-year decline, 2.4% miss)

- Adjusted EPS: $1 vs analyst estimates of $0.96 (4.1% beat)

- Full-year guidance: Organic net sales are now expected to be down 2% percent to down 1.5%, compared to the previous expectation of the lower end of the range of between flat and up 1%

- Operating Margin: 18.4%, in line with the same quarter last year

- Free Cash Flow Margin: 8.8%, down from 14.7% in the same quarter last year

- Organic Revenue fell 5% year on year (-1% in the same quarter last year)

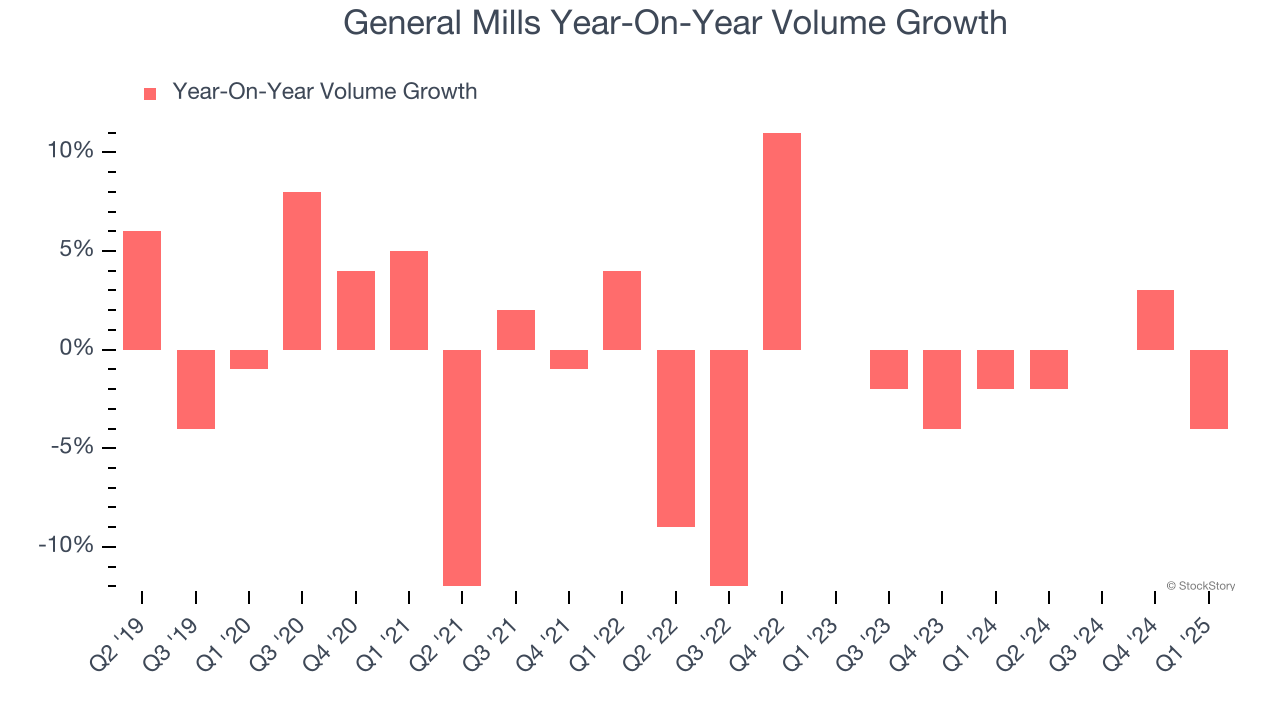

- Sales Volumes fell 4% year on year (-2% in the same quarter last year)

- Market Capitalization: $33.37 billion

“Our third-quarter organic net sales finished below our expectations, driven largely by greater-than-expected retailer inventory headwinds and a slowdown in snacking categories,” said General Mills Chairman and Chief Executive Officer Jeff Harmening.

Company Overview

Best known for its portfolio of powerhouse breakfast cereal brands, General Mills (NYSE:GIS) is a packaged foods company that has also made a mark in cereals, baking products, and snacks.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $19.64 billion in revenue over the past 12 months, General Mills is larger than most consumer staples companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. Its size also gives it negotiating leverage with distributors, allowing its products to reach more shelves. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, General Mills likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, General Mills’s 1.8% annualized revenue growth over the last three years was sluggish as consumers bought less of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, General Mills missed Wall Street’s estimates and reported a rather uninspiring 5% year-on-year revenue decline, generating $4.84 billion of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 2.5% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether General Mills generated its growth (or lack thereof) from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, General Mills’s average quarterly sales volumes have shrunk by 1.6%. This isn’t ideal for a consumer staples company, where demand is typically stable.

In General Mills’s Q1 2025, sales volumes dropped 4% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

Key Takeaways from General Mills’s Q1 Results

General Mills's organic revenue missed, causing its revenue to fall short of Wall Street’s estimates. Looking ahead, full-year guidance was updated as follows: "Organic net sales are now expected to be down 2% percent to down 1.5%, compared to the previous expectation of the lower end of the range of between flat and up 1%." Overall, this was a softer quarter. The stock traded down 3.3% to $58.45 immediately following the results.

Big picture, is General Mills a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.